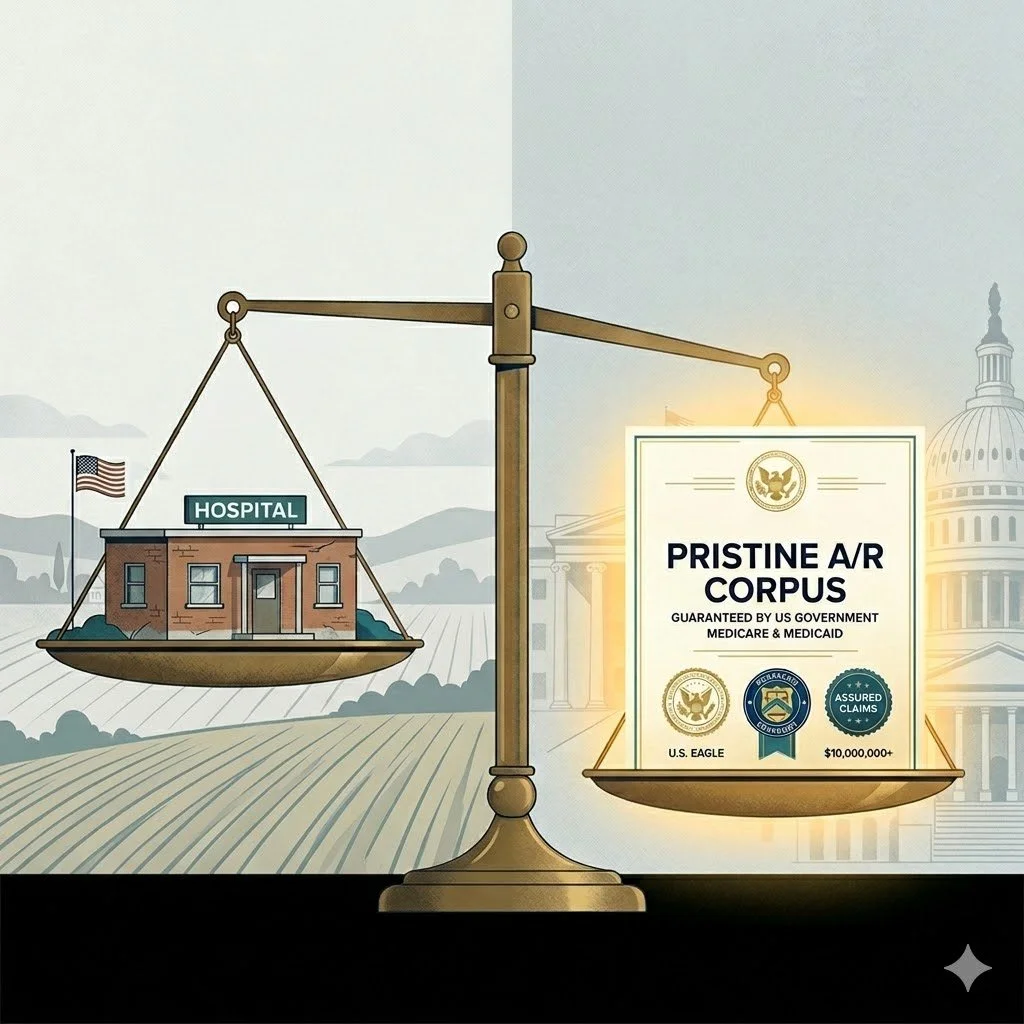

There is an absurdity at the heart of hospital finance that almost no one talks about. A rural safety-net hospital, carrying a payer mix dominated by Medicare and Medicaid, walks into a bank seeking a line of credit. The bank looks at the hospital's balance sheet — thin margins, negative days cash on hand, stressed working capital — and prices the loan accordingly. Punitive rates. Onerous covenants. Terms that would make a CFO wince. What the bank doesn't look at, because traditional lending frameworks are structurally incapable of understanding it, is the hospital's corpus of outstanding medical claims; even though the obligors of those claims (the federal government, state Medicaid programs) are among the most reliable payers in the financial system. The hospital's A/R has better credit than the hospital does. Yet the hospital is forced to borrow against its own weak balance sheet instead of the pristine creditworthiness of its payers. The market is functioning correctly with respect to the information it has. That information gap is costing vulnerable hospitals millions of dollars a year.

The "Opaque IOU" ProblemTo understand why this happens, you have to understand how traditional lenders see a medical claim. When a hospital submits a claim to Medicare, Medicaid or a commercial insurer, it creates an asset: a legal right to payment for services rendered. But to a conventional lender, that asset is essentially invisible. They can't reliably predict exactly when it will be paid, whether it will be paid in full, or what the probability of denial is. Without that predictability, they can't value it. And without valuation, they can't treat it as collateral. So they don't. They ignore the A/R entirely and instead evaluate the borrower standing in front of them — the hospital — on its own financial merits. A hospital with negative days cash on hand and a stressed line of credit looks, through this lens, like a distressed small business. The bank prices the risk accordingly. The cruel irony is, in the case of Medicare and Medicaid claims, that the payer on the other side of those "opaque IOUs" is often a government entity. The same government that issues Treasury bonds at the risk-free rate. A hospital holding $10 million in Medicare receivables is holding an asset backed by one of the most creditworthy obligors on earth — and being forced to borrow as if it held nothing at all.

A System That Punishes ComplexityThe traditional lending model doesn't penalize hospitals for being financially weak. It penalizes them for operating in an industry where the billing process is complicated. A straightforward commercial borrower — a manufacturer, a retailer, a logistics company — can pledge its receivables as collateral with relative ease. The cash flow is predictable, the payment terms are contractual, and the lender can model the risk. Healthcare receivables are different. Claim adjudication is opaque. Denial rates vary. Reimbursement timelines are inconsistent. The rules change. The complexity is real. But here's what that complexity doesn't change: the identity of the payer. A commercial payer's reimbursement timeline may be frustratingly slow. Its administrative processes may be maddening. But it pays. The federal government's obligation to reimburse a valid Medicare claim is not in serious doubt. The complexity is a feature of the billing process — not a reflection of the underlying credit quality. Rural hospitals, safety-net facilities, and independent practices feel this distortion most acutely. Their payer mixes are often heavily concentrated in government programs, which means their A/R is, in aggregate, among the highest-quality in the industry. And yet they face the worst borrowing terms — because their balance sheets are weakest, and because traditional lending has no mechanism to look past the balance sheet to the payer behind it. The result is a vicious cycle. Weaker balance sheets produce higher capital costs. Higher capital costs further weaken the financial position. A deteriorating financial position produces even worse borrowing terms on the next cycle. The hospital serves the same patients, delivers the same care, holds the same government-backed receivables — and falls further behind with each passing quarter.

Making the Invisible VisibleCapital Pulse was built to break this cycle by solving the core problem: the inability to value medical claims with enough precision to treat them as bankable collateral. Using AI and statistical learning models trained on large volumes of historical claims data, Capital Pulse predicts claim outcomes — payment timing, reimbursement amounts, denial probability — with accuracy ranging from over 92% to 95%, depending on payer type and claim category. That predictive precision transforms what traditional lenders dismiss as an opaque IOU into a known, quantifiable asset with a calculable value. Once a claim is accurately valued, the financing calculus changes entirely. The financier no longer has to price the risk based on the hospital's standalone creditworthiness. They can price it based on the creditworthiness of the payer: the federal government, a state Medicaid program, or a major commercial insurer. The hospital's thin margins no longer dictate the terms of the transaction. What matters is the credit quality of the entity that actually owes the money. This is what Capital Pulse's Healthcare Claims Scoring System — the HCSS — makes possible. By evaluating payer mix, denial rates, and reimbursement history to assign a standardized credit score to the claims portfolio itself, the HCSS makes the payer's creditworthiness legible to capital markets for the first time.

What Prime Financing Actually Looks LikeThe practical consequences of this shift are significant. When A/R is properly valued and treated as secured collateral, lenders can price the capital with the certainty of a secured instrument rather than assessing the hospital's standalone repayment risk on an unsecured basis. The result is financing priced at SOFR plus 200 to 350 basis points — roughly 5.6% to 6.9% annualized at current rates. Compare that to the emergency or punitive rates that distressed rural hospitals typically face, which can run 400 to 800 basis points higher than what large health systems pay for secured debt. For a hospital carrying $10 million in qualifying receivables, that rate differential is not a rounding error. It is hundreds of thousands of dollars annually; capital that could fund equipment upgrades, staff retention, or simply the working capital buffer that keeps the next payroll cycle from becoming a crisis. The Capital Pulse structure also enables 1-2 day reimbursement on qualified claims through a true sale of receivables, eliminating the reimbursement lag entirely — without the punishing discount rates of traditional factoring, and without adding a dollar of new debt to the balance sheet.

Stop Borrowing Against the Wrong Balance SheetHospitals have been paying an extraordinary premium for a billing complexity that is a feature of the healthcare system, not a reflection of their own creditworthiness or the quality of the care they deliver. The receivables on your balance sheet represent real services rendered to real patients, backed by real payment obligations from some of the most creditworthy obligors in the financial system. You have earned that revenue. The question is whether you access it on terms that reflect what you actually hold — or on terms that reflect only what a traditional lender can see. It is time to stop borrowing against your own balance sheet and start leveraging the credit of the entities that actually owe you money. To learn more about how Capital Pulse's AI-powered claims valuation can unlock the liquidity in your receivables portfolio, visit capitalpulse.com or contact our team directly.